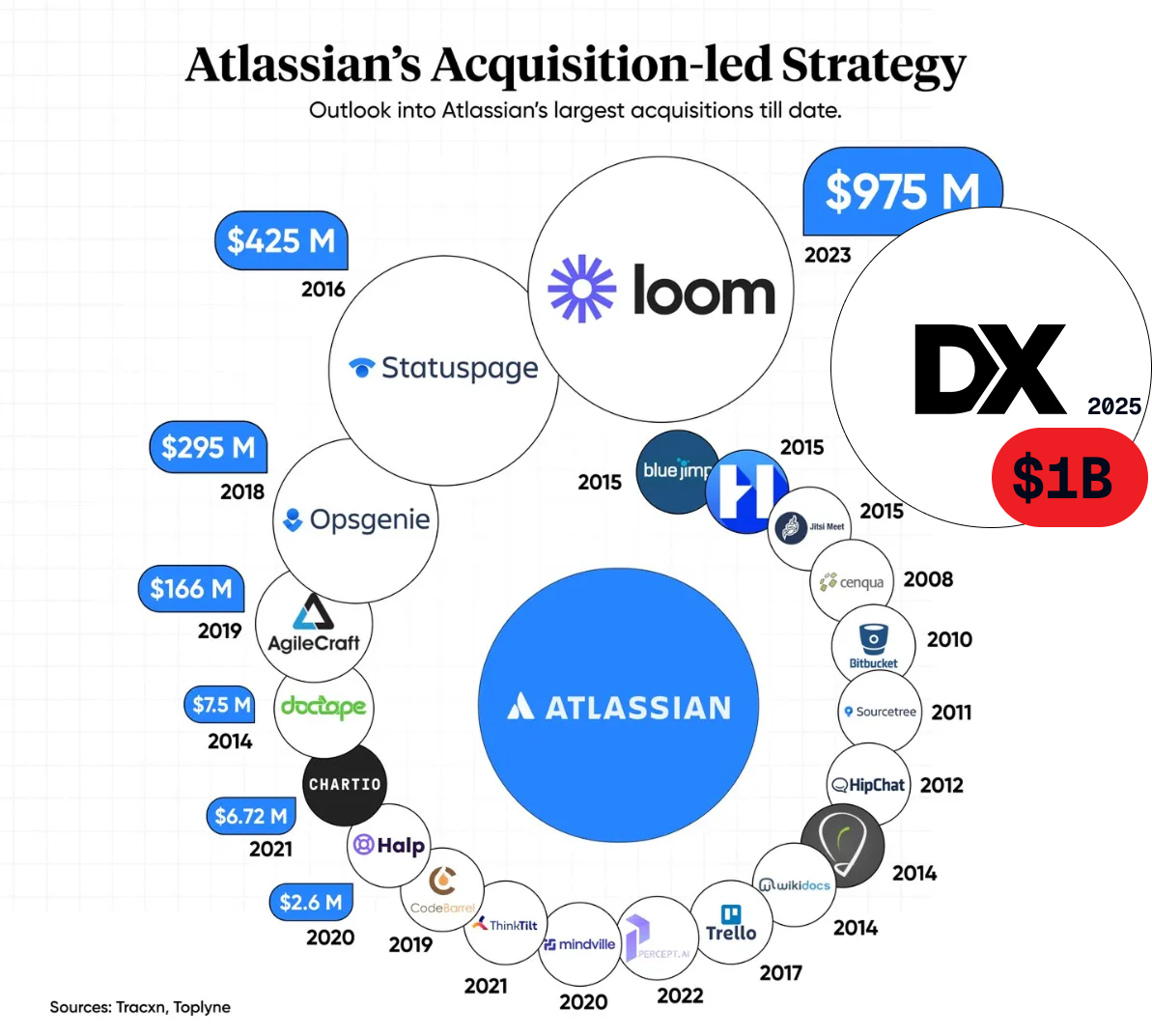

What Atlassian's $1B DX Acquisition Means for the Developer Productivity Market

Atlassian's AI platform play, how DX went $5M to $1B, and what this means for LinearB & other AI code review players

When a company hits unicorn status off of just $5 million raised, it’s a sign not just of stellar execution, but of an exploding market.

Atlassian’s largest-ever acquisition, $1 billion for developer productivity and intelligence platform DX, signals that the entire developer productivity market is entering a new phase.

With enterprises struggling to quantify returns on AI-driven software development investments, Atlassian’s new acquisition positions them to capitalize on a critical market gap. This acquisition isn't just about one company; it demonstrates that AI measurement capabilities and platform consolidation will reshape who wins and who gets left behind.

The implications extend far across the competitive landscape - creating potentially unexpected opportunities for companies like LinearB and exposing the looming specter of a Microsoft counter-acquisition.

$5 Million to $1 Billion

Two years ago, while working at fellow developer productivity platform LinearB, I wrote a memo warning that DX, newly out of stealth, was positioned to become a serious competitive threat. Their strategic execution stood out from the 20+ other small up-and-coming competitors.

DX was focused and highly intentional. The self-reinforcing elements of their strategy accelerated their progress towards unicorn status:

Strategic Angel Investors as Market Validators

Alongside traditional VCs, DX targeted multiple crucial strategic advisors and angels with both deep knowledge about leading engineering teams and massive influence to help DX go to market and build awareness.

DX’s bevy of developer productivity-aligned strategic angels and advisors included:

Nicole Forsgren: Researcher and thought leader - the influential force behind the industry-standard DORA (DevOps Research and Assessment) metrics framework, and much more

Gergely Orosz: creator of The Pragmatic Engineer, the #1 Technology newsletter on Substack with 1M+ subscribers

Will Larson: well-known CTO, author, and writer of the deeply admired tech blog Irrational Exuberance

Nat Friedman: former CEO of GitHub, 230k+ X followers, etc etc

Jason Warner: former GitHub CTO, influential investor, CEO & co-founder of Poolside AI).

These are just some of the well-known leaders and technology tastemakers who invested in DX. These weren't just investors; they are software engineering's most trusted voices, providing both credibility and distribution reach that no amount of marketing spend could replicate. The strategic value of these relationships is now even clearer: Jason Warner was just named to Atlassian's Board of Directors, creating a direct bridge between DX's investor network and Atlassian's strategic direction.

This pattern extends beyond just acquiring companies; it's about acquiring strategic networks. Jason Warner's appointment to Atlassian's Board immediately following the DX acquisition isn't coincidental. Successful acquisitions increasingly involve bringing key advisors and strategic thinkers into the acquiring company's governance structure(Reid Hoffman joining Microsoft’s board after LinkedIn’s acquisition is perhaps the most famous example), ensuring that the acquired company's strategic relationships and market insights become part of the acquirer's competitive advantage.

Founder-Led Thought Leadership That Actually Executed

While many founders talk about thought leadership, DX co-founder Abi Noda actually did it. He built his LinkedIn following to 25,000+ followers by consistently posting valuable content, launched a successful podcast, and published research with GitHub and other orgs central to developers’ perspectives. This is harder than it seems - it’s easy for busy founders to get distracted and fail to fully execute on such a strategy. But when done right, strong founder brands have massive leverage in deals and in shaping public narratives.

DX reinforced this strategy by building internal expertise and authority, encouraging all of their employees to share their perspective and content on LinkedIn, then strategically hiring yet another influential voice in engineering leadership and productivity with CTO Laura Tacho in 2023, and even picking up Deputy CTO and developer experience influencer Justin Reock in early 2025. They built up multiple in-house company ‘influencers’ on LinkedIn, and used their already established strategic alliances to validate, support, and distribute DX’s content and approach.

Together, their constellation of influence created an echo chamber effect. If you were at all interested in developer experience or engineering productivity, you would hear DX’s perspective. This second layer of reinforcement built upon and extended DX’s reputation, already sterling from their association with leading investors and allies.

Research-First Positioning

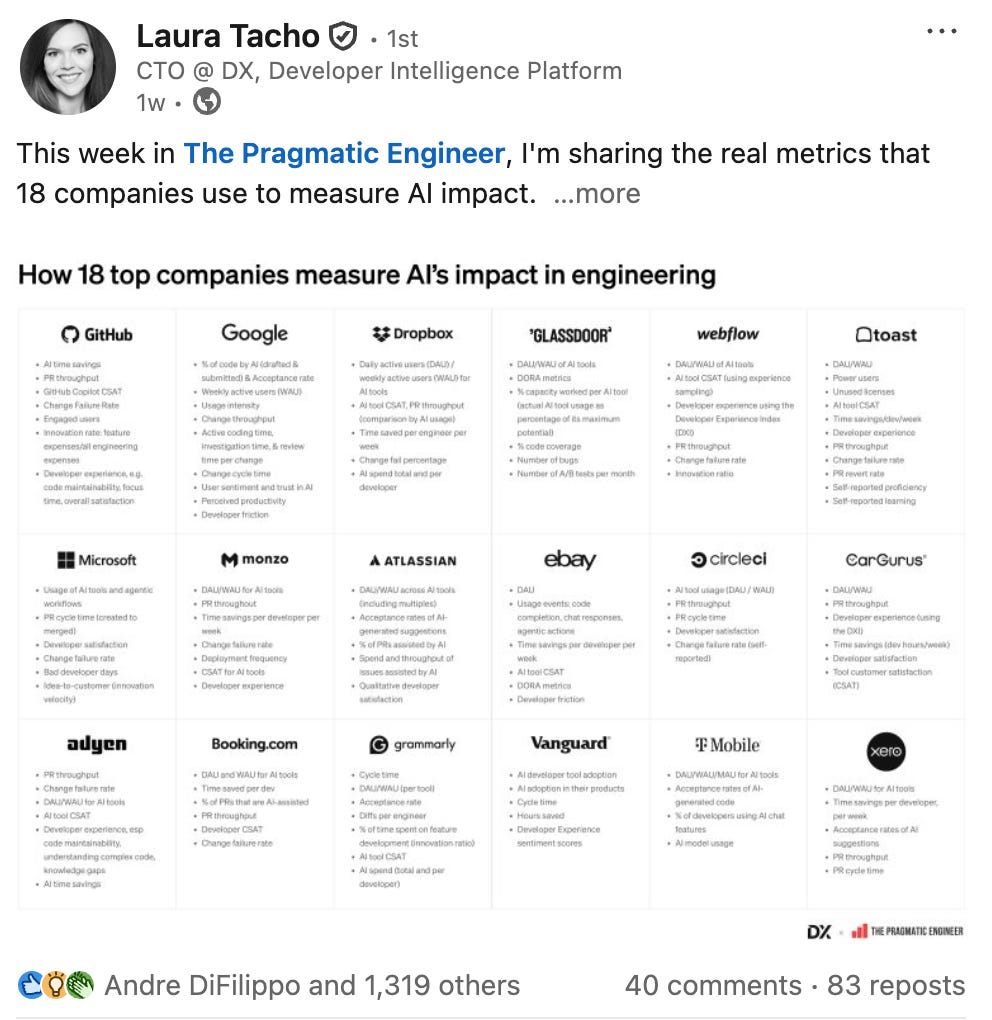

DX has positioned itself as the authority on developer experience measurement, not just another analytics tool. They have published papers, collaborated with GitHub on research, and established themselves as a source of truth for how to measure developer productivity, creating their own Core 4 framework, while associating themselves with some of the most well-known and cutting-edge software engineering teams and tools, such as their recent Claude Code integration. Increasingly, they have driven the conversation around developer productivity measurement.

Crucially, this research-led approach added further backing to their already established strengths:

Strategic investors: validation via authority of funders and attached brands

Thought leadership: narrative and persuasive argument

Research-backed: the numbers and science behind their perspective.

DX emerged from stealth in 2022, years behind established players such as LinearB, Jellyfish, Code Climate, and others. But DX knew that being late meant they needed advantages beyond product development. They systematically built authority and influence, creating a self-reinforcing strategy across their investors, leadership, and research.

Together, these approaches buttress one another - and their message lets them fly, to a rumored $40M+ in ARR in just 3 years out of stealth.

The Message Behind the Strategy

Above all, DX found product-market fit by understanding a fundamental tension in developer productivity tools. They recognized that developers resist being measured, that quantifying code impact requires more than just quantitative signals, and they entered the market with a qualitative-first, survey-driven approach focused on developer experience rather than pure productivity metrics.

This became DX's strategic wedge against established players. While competitors tracked engineering productivity through dashboards and metrics, DX positioned themselves as developer champions - exactly the audience they needed to win over to close enterprise deals. Their DORA-backed credentials provided the authority to back up this positioning, but the developer-first narrative solved a critical adoption problem that had plagued the category.

One persistent challenge for developer productivity tools has been overcoming the perception that they're surveillance systems imposed by management. There’s a reason many of us pushed back at McKinsey’s 2023 claims about measuring developer productivity, and companies can’t typically afford to alienate top technical talent.

DX defanged this concern from day one by framing their approach around improving developer experience rather than measuring developer output. They turned potential resistance into a competitive advantage, making it harder for metrics-focused competitors to win over developer stakeholders who influence purchasing decisions.

The pattern here extends beyond developer tools. Late entrants who become category leaders typically succeed not simply because they build better features, but because they execute better on market positioning, community building, and strategic partnerships. It’s part of what makes them so valuable.

Why $1B Makes Strategic Sense for Atlassian

Atlassian's willingness to pay $1 billion for DX isn't just about acquiring a developer productivity tool but positioning for what CEO Mike Cannon-Brookes calls "Engineering Intelligence for the AI Era."

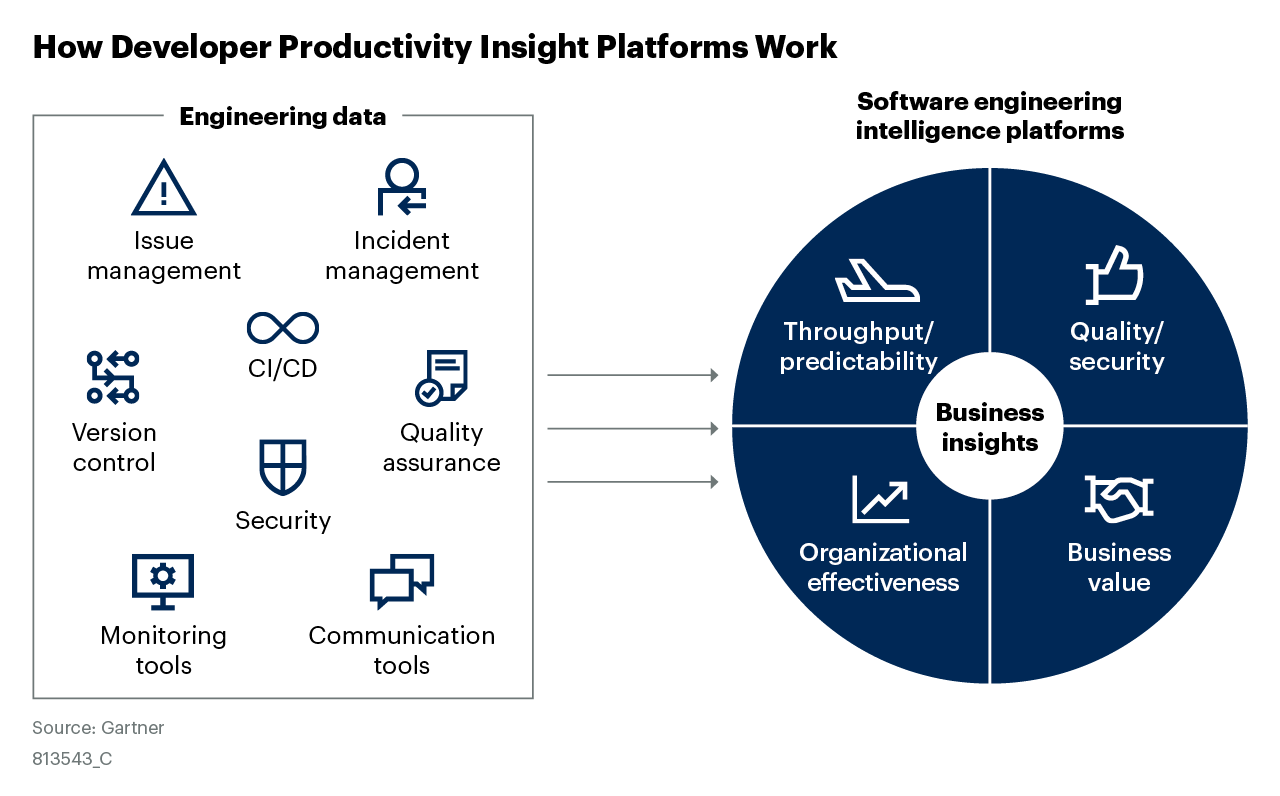

The timing couldn't be more critical. The broader DevOps market is exploding, growing from $12.5 billion in 2024 to a projected $37.3 billion by 2029. But within that growth, there's a specific gold rush happening around AI measurement and ROI tracking. As companies pour money into AI developer tools like GitHub Copilot, Cursor, OpenAI’s Codex, and Claude Code, they're struggling to answer basic questions: Are these tools actually making developers more productive? Which ones should we invest in? How do we measure ROI?

For Atlassian, this creates a powerful integration thesis. By combining DX's intelligence layer with Jira, Bitbucket, and their other tools, they can offer something no competitor can: complete software delivery intelligence within a single ecosystem, integrated with project management and their collaboration suite. With 300,000+ organizations using Atlassian tools globally and 90% of DX's existing customers already using Atlassian products, the distribution synergies are obvious.

This also follows Atlassian's recent pattern of aggressive AI-era investments. Earlier this month, they acquired The Browser Company for $610 million, signaling they're serious about building and adding AI-native experiences across their platform. The DX acquisition completes the picture. Atlassian now has both AI-powered tools and the intelligence layer to measure their impact.

Increasingly, this puts pressure on Microsoft, GitLab, and other platform vendors to acquire or develop similar capabilities to avoid being left behind. Microsoft poses the most potent threat with its integrated GitHub, Azure DevOps, and Teams ecosystem, but lacks the specialized developer productivity measurement capabilities that DX brings. This gap gives Atlassian meaningful differentiation in the race to quantify AI development investments. I expect Microsoft/GitHub to make a counter-acquisition in the next 18 months.

The DX deal also positions Atlassian ahead of project management competitors like Asana and Monday.com, which lack developer-focused tooling and productivity analytics. As enterprises increasingly demand integrated platforms over point solutions, Atlassian's combined offering of project management, collaboration, and developer intelligence becomes significantly more defensible.

This integrated approach addresses enterprise decision fatigue around developer tooling, where organizations managing dozens of development tools increasingly prefer consolidated platforms. The 90% overlap between DX's customer base and Atlassian's existing users enables Atlassian to serve enterprises that want fewer vendor relationships and less integration complexity, not more specialized point solutions.

The timing reflects a critical enterprise need: IT spending on AI development tools now exceeds traditional productivity software costs by 300-400%, yet most organizations struggle to measure returns on these investments. DX's analytics platform addresses this measurement gap, helping justify and optimize AI-focused development expenditures.

Market Consolidation Patterns

This isn't the first major deal in the space, and it definitely won't be the last.

Harness has been particularly active, acquiring Propelo (now known as Harness Software Engineering Insights) in January 2023 and Armory's assets in January 2024. These deals signal that platform companies are moving aggressively to consolidate specialized tools rather than build competing solutions in-house.

The math behind this trend is compelling. The DevOps market is projected to reach $43.17 billion by 2030, growing at a compound annual growth rate (CAGR) of 21.76%. But within that growth, there's increasing pressure for consolidation, and AI’s influence is accelerating everything, while expanding the potential pool of rewards. Enterprise buyers are tired of managing dozens of point solutions and want integrated platforms to handle their entire software delivery lifecycle. They’re also desperate to quantify and track the massive capex spend they’re putting into AI.

This creates both opportunity and urgency for remaining independent players. Buyers want alternatives to vendor lock-in, creating openings for cross-platform solutions. However, the window for strategic exits is narrowing as the biggest platform players make their moves, and valuations reach a fever pitch, signaling the potential for the AI bubble to deflate.

The choice facing most remaining companies is stark: get acquired by a platform player, or build enough scale and integration to become a platform themselves. Very few will succeed at the latter, so we should expect additional acquisitions over the next 12-18 months.

This is particularly interesting because each major acquisition changes everyone else's competitive landscape. DX being absorbed into Atlassian's ecosystem means they'll likely stop pursuing integrations with competing platforms like GitHub and GitLab. That creates openings for other players who can serve multi-platform organizations.

Impact on the Developer Productivity Landscape

DX’s acquisition represents stellar validation for the developer productivity space. A $1 billion exit proves that what was once seen as a nice-to-have category is actually a strategic imperative for enterprises seeking to unlock AI-enabled engineering. The return to higher valuation levels also signals that the market has recovered from the 2023 downturn, a marked positive for the entire industry. Previously, only fully AI-native companies had been getting these kinds of price tags.

Interestingly, the acquisition also creates several strategic advantages for DX competitor LinearB and other developer productivity tools:

Ecosystem Constraints Create Opportunities

DX is now locked into the Atlassian ecosystem. Atlassian will use them to solve Atlassian's problems. They'll optimize for Jira, Bitbucket, and Confluence integrations but likely won't pursue deep partnerships with GitHub, GitLab, or other competing platforms. This constraint creates a significant opportunity for cross-platform solutions like LinearB, which can serve multi-vendor environments that DX can no longer easily address within Atlassian's ecosystem.

AI Code Review Differentiation

LinearB has positioned itself well in the expanding AI code review market through its platform approach, but faces formidable competition from specialized players. The space has attracted significant venture investment, with CodeRabbit hitting a $550 million valuation and emerging as a developer favorite through its sophisticated multi-agent architecture that creates dynamic task graphs. Meanwhile, Qodo Merge leads the open-source segment, and GitHub Copilot leverages native integration advantages despite mixed early reviews. Graphite has also developed a cult following (and I had a great conversation with their co-founder on Chain of Thought).

LinearB's differentiation lies in combining AI code review with broader workflow automation and productivity measurement, an integrated approach that will prove valuable in the post-DX acquisition landscape. While pure-play code review tools excel at catching bugs and style issues, LinearB's platform can connect code quality improvements to broader developer experience metrics and business outcomes. This positions them favorably for enterprise customers seeking consolidated tooling rather than managing multiple specialized vendors.

However, execution remains critical. The AI code review market is moving fast, with well-funded competitors rapidly improving their capabilities and new startups emerging seemingly every week. LinearB's success will depend on seamlessly integrating its code review features with its existing productivity platform while staying on the cutting edge of AI software development workflow governance, particularly with the rise of AI agents.

As I’ve written before, faster code reviews are perhaps the highest leverage point for improving your team’s software delivery speed.

Market Segment Opportunities

LinearB's strategic positioning with its new AI adoption-focused Essentials package at $19/month captures smaller teams and growing companies that prefer flexibility over Atlassian's increasingly enterprise-oriented approach. As DX gets absorbed into a larger, more complex sales process, there's an opportunity to capture customers who want simpler, more focused solutions.

The broader competitive reshuffling also creates urgency for other players. GitHub, which has been organically building developer productivity features, may feel pressure to make an acquisition to compete with Atlassian's integrated offering. GitLab, similarly, might look to acquire measurement capabilities rather than build them in-house.

My prediction: we'll see 2-3 more major acquisitions in this space over the next 18 months as platform players move to establish their positions before the market fully consolidates. Alongside LinearB, Jellyfish is likely to be a key target and could be paired with one of the AI-native code review startups to flesh out a platform ecosystem. Multiple smaller software development analytics startups, such as Swarmia, Sleuth, Allstacks, or Hivel, could also be targets for acquisition.

Pattern Recognition Across Markets

This acquisition fits a pattern we’ve seen across multiple industries: specialized tools getting absorbed by larger platforms during periods of rapid technological change.

In marketing technology, we saw HubSpot acquire dozens of specialized tools to build its integrated platform. In security, Palo Alto Networks has been on an acquisition spree, buying everything from cloud security to identity management companies. The same pattern is now playing out in developer tools.

The driving force is always the same: customers get tired of managing dozens of point solutions and start demanding integrated experiences. Platforms race to consolidate the most valuable specialized tools before competitors do. The result is that independent tools that might have thrived in a fragmented market get absorbed into larger ecosystems.

This acquisition provides a useful framework for thinking about strategic positioning for founders in adjacent categories such as design tools, data platforms, or infrastructure management. Are you building features that a platform company could replicate? Or are you building strategic advantages (community, research authority, unique partnerships) that would be valuable for a platform to acquire rather than compete with?

The window for strategic exits in many categories may narrow faster than most founders realize. AI is accelerating product development cycles, making it easier for platforms to spin up competing features. But it's still hard to build community, authority, and strategic relationships on top of happy customers, precisely what made DX valuable enough for a $1 billion acquisition. It’s also why the Dev Interrupted media brand I built for LinearB has proven so valuable for them - both in their own customer acquisition and likely in the case of LinearB’s own eventual acquisition.

Looking Ahead

Developer productivity tools have officially moved from a nice-to-have to a strategic imperative in the AI era. The DX acquisition proves companies will pay significant premiums for tools that help them understand and optimize their engineering investments.

But this is just the beginning of a broader market transformation. In the next few years, the platforms that can provide measurement and optimization across the entire development toolchain, not just within single ecosystems, will win.

For engineering leaders, this means the tools you choose today will increasingly determine your strategic flexibility tomorrow. Betting on single-vendor solutions might give you better integration, but it could also lock you into platform - or AI models - that may not serve your needs as the market evolves.

The lesson for founders and investors is clear: strategic positioning matters just as much as product development in rapidly growing markets. DX didn't win because it built substantially better analytics; it won because it built better relationships, authority, and market positioning.

Or, tell me what I got wrong 😉

Disclosure: Author holds LinearB equity from previous employment. This post was for informational purposes only and is not intended as financial advice.